The Great Supply Chain Squeeze Demands Smarter Sourcing Decisions

Sponsored Content

Will your diversification strategy strengthen resilience – or expose you to hidden risks in another part of the supply chain?

Supply chain leaders are having to make tougher decisions. Tariffs, conflict, regulatory fragmentation, geopolitical realignment, environmental shocks and human rights risks are becoming structural features of the global operating environment.

Costs are rising, lead times are under pressure, supplier concentration is a growing concern, and logistics networks are being tested by events that often outpace traditional planning cycles. For many businesses, the instinctive response is to diversify: find new suppliers, build alternative routes and reduce dependency on single markets.

But diversification only strengthens resilience if companies understand where their footprint is moving, how those locations connect to the wider network, and what hidden risks they might be exposed to as they reroute their supply chains.

Supply chain risk is rising

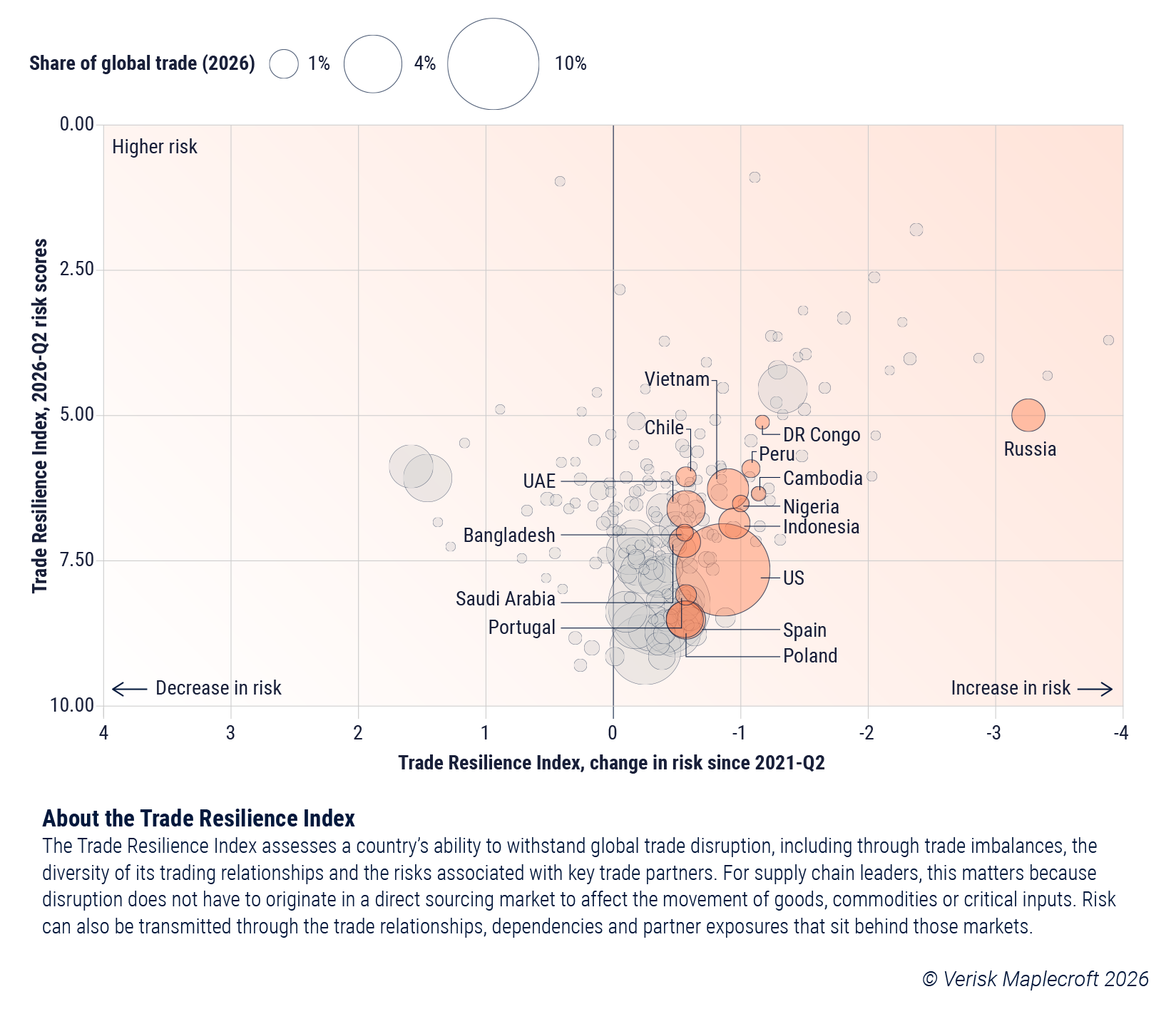

According to Verisk Maplecroft’s data, supply chain risk is rising globally. Over the past five years, trade resilience has deteriorated in 157 countries, which together account for more than 90% of global trade. This data is taken from Verisk Maplecroft’s Trade Resilience Index, featured in their Supply Chain Risk Outlook 2026, which assesses a country’s ability to withstand global trade disruption, including trade imbalances, trading relationship diversity and risks associated with key trade partners.

Disruption does not always arise in the locations where you have direct exposure. Instead, it can spread through the trade relationships, dependencies and partner exposures behind those markets. A supplier may appear stable in isolation, while the wider network around it is becoming more vulnerable.

Cost, quality, capacity and lead times remain essential, but companies also need to understand how geopolitical, regulatory, security, environmental and human rights risks are changing the assumptions behind their choices.

Look beyond headline chokepoints

The recent disruption to shipping through the Strait of Hormuz shows how quickly conditions around a major chokepoint can change, forcing companies to rethink routes, freight options and contingency plans.

But risk is not confined to the world’s most visible chokepoints. Verisk Maplecroft’s data shows that approximately one-third of the world’s busiest ports and airports are vulnerable to disruption from at least one type of operational shock, including geopolitical and conflict factors, environmental risk and domestic security threats.

A business might diversify its supplier base, but still rely on ports, airports and logistics hubs where multiple risks overlap. The biggest vulnerability might not be located in the main production facility. Sometimes it’s hidden in the infrastructure that connects goods to customers. Or there may be a need to understand what happens when disruption forces a shift from, for example, sea freight to air freight.

Companies therefore need to identify the critical infrastructure nodes they depend on, monitor the risks affecting them, and understand how disruption could affect sourcing, contracting and inventory decisions.

Diversification has become more complex

Geopolitical risk has moved diversification from an efficiency exercise to a boardroom priority. The Supply Chain Risk Outlook identifies Thailand, the Philippines, Argentina, Uruguay and Chile as creating new options for the next phase of diversification. But these are not simple, interchangeable replacements for established sourcing hubs.

Each market brings a different mix of production capacity, market openness, regulatory strength, labour-risk trajectory, logistics exposure and geopolitical context. The opportunity lies in assessing which sectors those markets can support, where supplier relationships can be built before demand spikes, and how external risks could affect execution.

Forced labour, conflict exposure and human rights risks are also becoming operational and market-access issues, not just reputational or compliance concerns. Companies may face shipment detentions, import restrictions or legal exposure even when the risk sits several tiers beneath the surface of the supply chain.

The key question is what new risks the diversification strategy creates – and how quickly the business can detect if conditions have changed.

We need a live view of risk

Annual risk reviews and single-point contingency plans are unlikely to keep pace with constant instability. Companies need to integrate external risks into decision-making, strengthen their risk radar with better data, and move towards a continuous risk intelligence loop that tracks how exposure changes as markets, suppliers and routes evolve.

Not every shock can be predicted. But better-informed decisions can help companies identify where the supply chain is vulnerable before disruption cascades into higher costs, longer lead times, compliance failures or lost market access.

The organisations best placed to navigate this environment will be those that can see how risks connect – enabling them to make smarter sourcing decisions before the next shock emerges.

Get Verisk Maplecroft’s Supply Chain Risk Outlook 2026 to explore where trade resilience is weakening, where hidden vulnerabilities are building, and where new sourcing opportunities are emerging.