A TCO Approach to Contract Labor: Evaluating Billable Wages

By Leviticous “Vic” Cleveland

Welcome back to our ongoing discussion of understanding billable wages. To counter the rising costs of contract labor throughout the Gulf Coast region, many companies like ours are looking for ways to reduce costs, or at least lessen the impact of cost escalations. More specifically, my team and I have undertaken a total cost of ownership (TCO) approach to understand cost structures and influence our rising demand for contract labor.

In the first installment of this discussion, I diagrammed the components of bare and billable wages, such as taxes, fringes and benefits. Understanding these components is essential in understanding what you’re paying for and building an effective should-cost model. That’s what this installment is all about — evaluating billable wages.

I have found it helpful to utilize several different approaches: should-cost modeling, internal market analysis and external market comparisons.

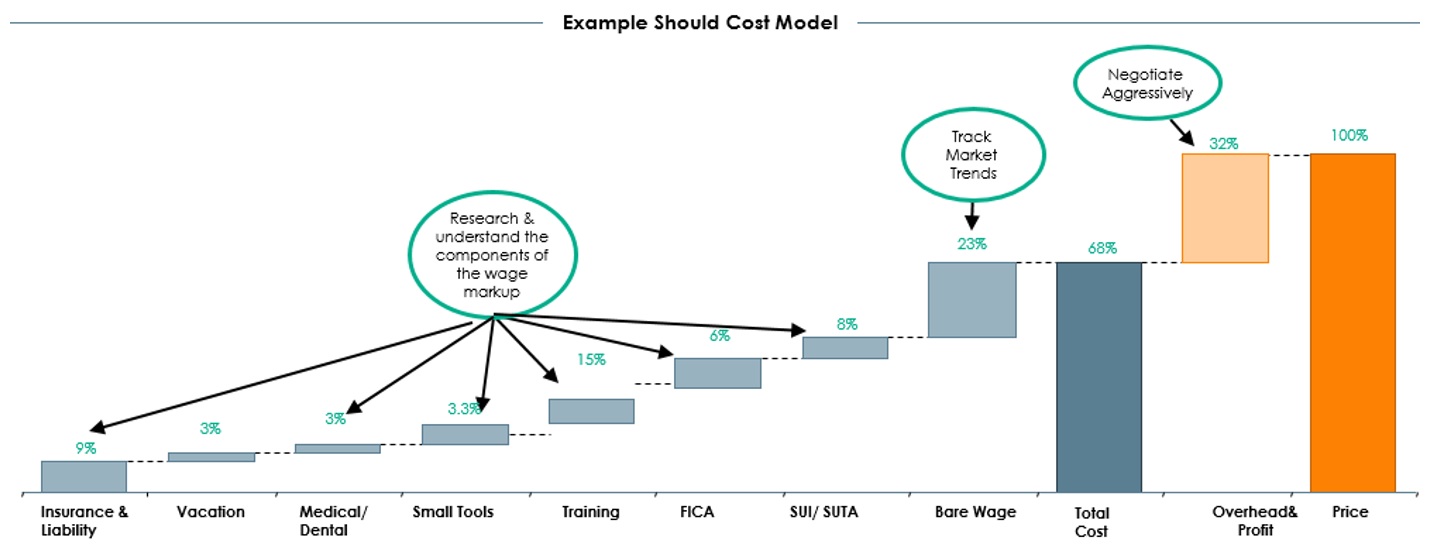

Should-cost modeling. A good place to start, a should-cost model is a tool used to help determine the price you “should” pay for a product or service. In creating a should-cost model, you are essentially behaving as if you are the provider or manufacturer of the product or service. Use the model to evaluate the price you should pay compared to the price you are paying.

For example, regarding labor wages, first reference the components of billable wages discussed the first installment to create a transparent view of the wage. Then, factor in a modest percentage to cover overhead and profit. You have now created a should-cost markup that you can use to evaluate other proposals. (See below.)

Creating should-cost models requires work, as you will need to research cost elements that are not always readily available. However, you will find that should-costing can also be a helpful tool when conducting negotiations with counterparties.

Internal market analysis. When conducting an internal market analysis, I am always surprised at the findings. This is particularly true since our internal data-mining tools have improved and generate greater data transparency.

Data-visualization tools have become in vogue. After two years of learning to navigate a few of them, I see what the fuss is about. Ten years ago, our data was more isolated, and our teams tended to work in silos to some degree. We might contract for a service in one area at rate X, and a similar service in another area might be contracted at rate Y. As time-keeping and gate-log tools have improved, so has our visibility of the associated data.

The data-visualization and business-intelligence tools available on the market today have made this process easier. These platforms allow you to upload large sets of data and instantly create visualizations to pinpoint gaps to address. For example, when using one of these platforms, I uploaded a portfolio of wage-rate proposals from multiple suppliers. I subsequently created a heatmap that I used evaluate the ranges of bare wages, markup and billable wages offered. (See below.) These data-visualization tools are not free, but some offer free trials.

External market analysis. Depending on your sourcing strategy, an external market analysis might be appropriate. If you have determined that tendering the service in question is the right approach, then supplier responses to your RFX will reveal the going billable-wages rates. In this scenario, it can also be helpful to have access to an independent source of market-intelligence data.

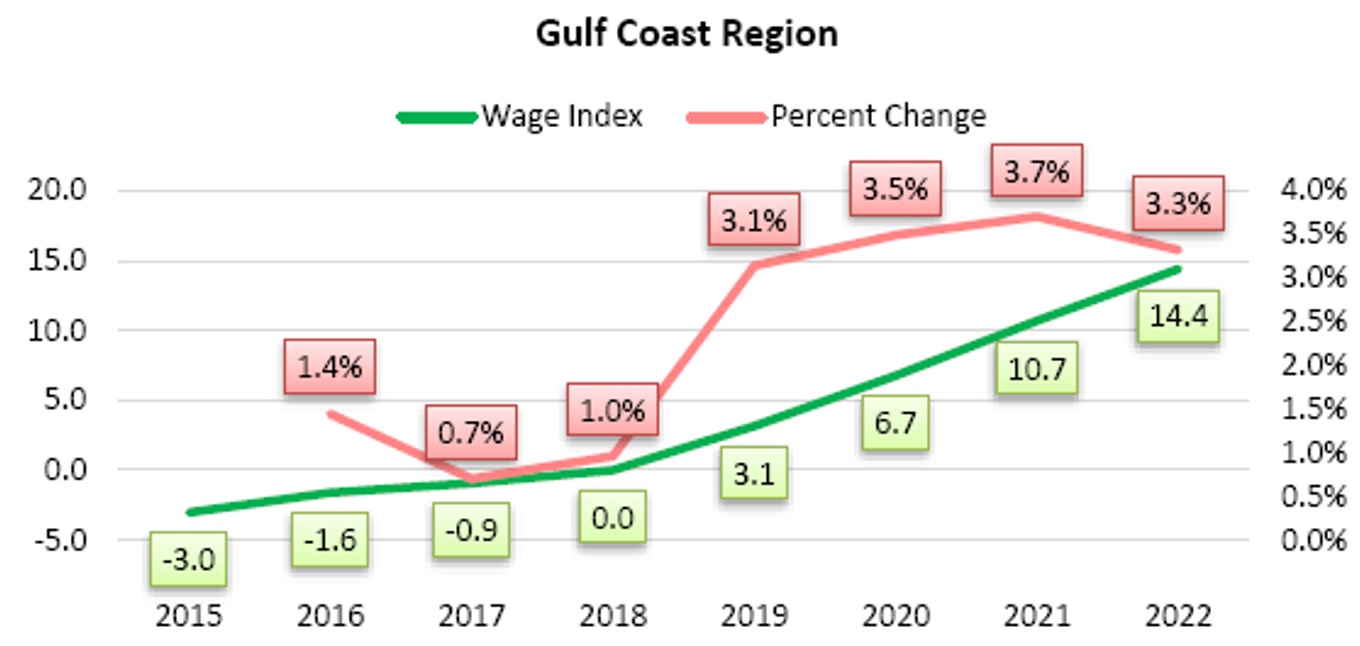

Many firms provide labor-forecasting data. The firms query the market by conducting monthly interviews with suppliers to determine current wages. They use modeling techniques and wage factors to create a profile of forecasted wages in the region. (See below.)

As no data source is perfect, I suggest coupling this market-intelligence data with your own should-cost model during your evaluation to provide a more optimal evaluation. For example, assume an incumbent welding supplier has presented a proposal for a wages rate increase. Construct a should-cost model to determine the cost you should pay for this service. Next, review internal data to evaluate costs paid to other suppliers providing the same or similar welding services. Lastly, using external data, contract the supplier’s proposal to current market rates. Try to understand how rates are trending.

Utilizing these three tactics should provide perspective to properly evaluate the proposal. In the next installment, we will begin exploring other means of influencing the cost of contracting, such as contract pricing methods and remuneration.

Leviticous “Vic” Cleveland is a senior category manager for services contracting at Motiva Enterprises LLC in Houston.